Investment Team Handelsbanken Wealth

27 Mar 2026 8

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

It’s fair to say that the first quarter of 2026 has been a volatile period for markets, but it’s especially true for UK government bonds (or gilts).

In the opening weeks of the year, the market narrative was one of improving global growth and falling inflation; a benign and supportive backdrop for government bonds.

While this was the narrative for global markets, it was particularly applicable to the UK’s economic backdrop. UK growth, or the lack thereof, was looking like it had troughed, and there were already embryonic signs of a developing recovery showing up in a raft of data sources, including economic activity surveys (not a major improvement, but a recovery nonetheless).

The UK gilt market was reacting positively to this; yields were falling (meaning that prices were rising), Rachel Reeves’ fiscal headroom was building, and the market was expecting the Bank of England to cut interest rates twice more this year.

The Iranian escalation subsequently set this market narrative on its head. Along with oil, government bonds have been one of the most volatile asset classes ever since.

Why government bonds have been impacted by the Iran war

Commodity markets have been one of the chief theatres in which the Iran war has been played out. Prices here have spiked, especially for oil and gas given the current tensions in the Middle East have ‘effectively’ closed the Strait of Hormuz, through which circa 20% of the world’s oil, liquefied natural gas and fertilisers usually pass.

This has understandably manifested as concerns around how much the closure will impact both global growth and the near-term trajectory for inflation, especially in regions like Europe and the UK. Our economy, like that of our European neighbours, has a much higher sensitivity to oil and gas prices than, say, the US. As we’re far from being energy self-sufficient, we remain major importers of both oil and gas.

This has played out in bond markets with steeply rising market expectations for inflation alongside a complete reassessment of what path central banks are now likely to set interest rates upon in 2026.

In the case of the UK, interest-rate expectations have moved from pricing in two interest-rate cuts for this year to, at one point earlier this week, four potential interest-rate increases! By bond market standards, this is a seismic reassessment in such a short space of time. This has led to bond yields rising steeply (meaning their prices have retreated).

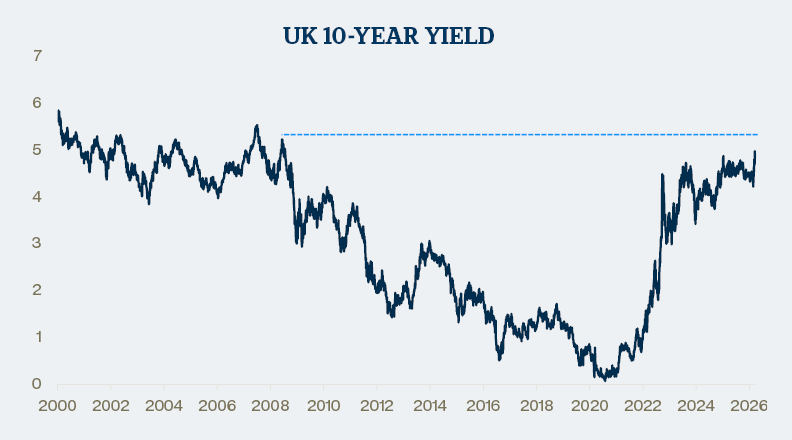

Between the onset of the Iran war on 28 February, and the time of writing (26 March 2026), the yield on two-year UK government bonds had risen by 84 ‘basis points’ (meaning 0.84%), while the yield on 10-year gilts had climbed 54 basis points (0.54%), and the yield on 30-year gilts was up 43 basis points (0.43%).

These are large moves. To put this into context, the yield on 10-year gilts hasn’t been this high since 2008 in the aftermath of the global financial crisis.

Source: Bloomberg as at 26 March 2026

How we’ve responded to this in our client portfolios

Given the size of the moves in government bond markets, especially in the UK, our multi asset class portfolios haven’t been completely immune to this repricing. Naturally, the impact is most notable in our lower-risk portfolios, such as Defensive and Cautious, which have the highest weighting to bond markets.

However:

We are firmly of the view that, while the evolving backdrop now means the Bank of England is unlikely to cut interest rates twice this year, we don’t believe it will raise rates four times either, particularly given the negative impact that recent commodity prices will have on UK economic growth.

Our assessment is that UK government-bond valuations are beginning to look attractive once more through our long-term lens. Whilst volatility may persist in the asset class in the near term, we think yields at these levels represent a compelling medium to long term opportunity. Consequently, this week we bought gilts with a short to medium-dated maturity profile as we think that’s where the best value has emerged in recent weeks.

This means that our portfolios have now gone from being ‘neutral’ on UK government bonds (in line with our long-term average) to being marginally overweight.

The value of investments and any income from them can fall and you may get back less than you invested.

Handelsbanken Wealth is a trading name of Handelsbanken Wealth & Asset Management Limited which is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business and is a wholly-owned subsidiary of Handelsbanken plc. Tax advice which does not contain any investment element is not regulated by the FCA. This document has been prepared by Handelsbanken Wealth for customers/potential customers who may have an interest in its services. The provision of this information does not constitute tax, pensions or investment advice.

Tax rates and legislation are subject to change. We cannot guarantee to inform you of any such changes and Handelsbanken Wealth accepts no responsibility for any inaccuracies or errors. Any levels of taxation referred to depend on individual circumstances and the value of tax reliefs are those which apply at 19 February 2026.

The value of the pension received when taking benefits from a pension will depend on various factors including, but not limited to, contributions made, charges and fees, tax treatments, annuity rates, investment performance. Professional advice should be taken before any course of action is pursued.

This does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. Handelsbanken Wealth cannot accept responsibility for the consequence of any action taken or failure to take action by a reader on the basis of the information provided. When we provide advice in relation to investment, our own investment management services will usually be recommended. When advice on pensions or other products outside an investment management relationship is required, we will recommend products chosen from a limited selection of providers that have been appointed on the basis of its judgement in their quality of service, investor protection, financial strength and, if relevant, their financial performance. As a result, any advice given by Handelsbanken Wealth in respect of retail investment products will be restricted as defined under the FCA rules.

This document has been issued by Handelsbanken Wealth.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340