Investment Team Handelsbanken Wealth

30 Apr 2026 10

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

While war in the Middle East has sent oil prices spiralling and reversed interest-rate expectations, it’s also triggered a ‘bull market’ in US and emerging market technology stocks and the re-emergence of the totemic Magnificent 7 stocks.

It took just a week from the announcement of a ceasefire between US/Israel and Iran on 8 April for the US stock market to hit new record highs. The S&P 500 Index of US companies closed above the 7,000 mark for the first time in its history on 15 April, amid what was another strong start to US earnings season. In doing so, the world’s most important stock market index broke free of the narrow trading range in which it had been contained since October 2025.

With the exception of a brief dip lower in the last week of March, the S&P 500 Index had previously remained within 350 points of the 7,000 ceiling for well over six months.

Hidden intrigue

Of more consequence for investors is what’s been developing beneath the surface of the index. Although it’s technology and hardware stocks that are now stealing all the headlines, there’s a significant dispersion of returns within the market.

This has been driven by investors previously shifting their economic expectations and rotating into long ‘unloved’ sectors such as industrial, manufacturing, resources, energy and utility companies at the expense of the Magnificent 7, other technology stocks, and those service-based companies whose business models looked most vulnerable to the rising wave of AI adoption.

Passing the baton…

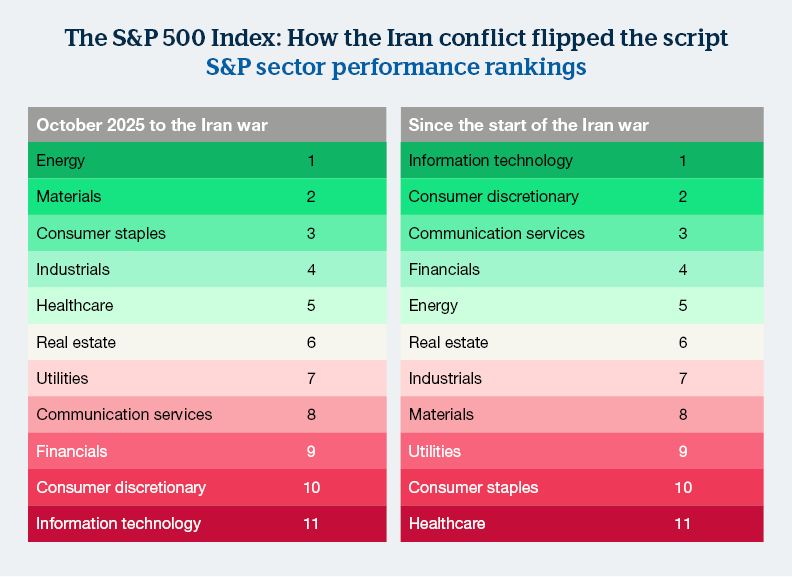

While the S&P 500 remained resilient at a headline level from October 2025 to February 2026, leadership notably shifted away from its largest underlying sector, technology, and from the consumer discretionary sector (which includes the likes of Amazon and Tesla). These sectors had dominated US stock market performance in 2024 and were highly prominent until late in 2025 when investors began to diversify by looking for value in a broader, more ‘cyclical’ market (meaning one more driven by the robust US economic backdrop).

By November of 2025, the US AI giant Anthropic had released the latest generation of its Claude AI (Opus 4.5). Its arrival, and a rash of smaller AI launches that followed in early 2026, shook US software stocks – a core constituent of the technology sector – with fears that business-to-business service models would become obsolete overnight.

At the same time, the first quarter of 2026 saw investors questioning the potential future returns on the prodigious levels of capital expenditure being committed by a handful of so-called ‘hyperscalers’. Quite understandably, investors feared both whether such Herculean outgoings could ever return a profit, and whether their continued presence would drain those companies’ ability to return cash to shareholders via buybacks and dividends.

Old-fashioned tastes…

With investors fretting over the market’s talismanic technology stocks amid signs that the US economy was experiencing a ‘cyclical re-acceleration’ – aided in part by prior interest-rate cuts from the US Federal Reserve – a new appetite for ‘old economy’ stocks emerged. Consequently, the US market was being led by the energy, materials, and industrial sectors.

A little counterintuitively, consumer staples stocks – traditionally ‘defensive’ holdings – also performed well as investors focused on finding unrecognised value. Meanwhile, they continued to punish those companies potentially disrupted by AI, while simultaneously betting on those firms that could see the best margin expansion as a result of adopting the same new technology.

So abrupt were these shifts that by February of this year, for the first time since 2022, the price to earnings (P/E) multiples of the technology and consumer staples sectors were identical. This meant that, for a brief moment in time, retailers like Walmart and Costco, which subsist on tiny margins, and household goods producers like Procter & Gamble, Coca-Cola, and Philip Morris, which have similarly tight margins, were valued the same as the likes of Nvidia, Apple or Microsoft, despite the latter having profit margins that are four times the size of those enjoyed by the former!

Elsewhere, part of the pre-Iran paradigm, which saw technology stocks retreating and economic fundamentals coming the fore – namely falling interest rates, muted inflation and robust economic growth – was the re-emergence of US smaller companies. After a long period in the shadows, they began to outperform their larger peers. This was thanks to there being relatively few smaller-company technology stocks, and the increased expectations for smaller company earnings that always accompany a strengthening domestic economy (because smaller companies tend to be more domestically focused).

Iran conflict flips the script (again)

The onset of the US/Israel war on Iran on 28 February sent reverberations throughout global markets, prompting investors to ‘rotate’ once more.

One of the most immediate effects was what might be described as a ‘stagflationary pivot’ ie investors suddenly became worried that inflation would rise and growth would slow.

This saw cyclical sectors, such as materials and industrials, giving back their prior gains as investors fretted over the outlook for continued economic growth. Energy was the only sector to make gains as Brent crude rose above $100 a barrel (and stayed in that neighbourhood for the next seven weeks).

With the announcement of a ceasefire, this trend quickly reversed as growth concerns faded once more and inflationary worries eased.

Two months after the start of the war, amid a period of ceasefire punctuated by bombastic US rhetoric, this rotation is most apparent in the US technology sector. Having been shunned by investors – and ranking as the worst-performing sector in the first two months of the year – tech stocks found some price stability during the opening weeks of the conflict.

This partly reflects the margin structure of most technology stocks – they’re far more resilient to rising energy costs as they can simply pass these along to their customers.

Following the announcement of the ceasefire on 8 April, it’s technology stocks that have rallied the most above their pre-war levels, fuelled by a cocktail of robust earnings growth, AI spending suddenly being seen as a positive, and US investors returning in great numbers to ‘buy the dips’. This has propelled the S&P 500 to its new record highs.

Meanwhile, traditional defensive sectors have been among the worst performers since the start of the Iran war with US consumer staples, utilities, and large-cap healthcare stocks all still below their pre-war levels.

This is largely explained by changing interest-rate expectations: these sectors are among the most sensitive to changes in interest rates. Consequently, they’ve suffered as interest-rate expectations have broadly returned to ‘higher for longer’, due to the impact of the war in the Middle East.

Daylight emerging

Within the sprawling US technology sector, it’s semiconductor (microchip) stocks – namely hardware companies – that have enjoyed the best progress. The onset of a ceasefire, however fragile, has helped hardware companies to pull away from their software peers as investor attention has returned to the ‘AI buildout’ narrative.

Driven by sustained demand for AI infrastructure in the form of datacentres and the endless cabling, power systems, and computing chips they require, a myriad of major hardware names have already provided bumper earnings reports, and optimistic guidance, with powerful ‘read across’ for other companies in the same niche.

Software companies, meanwhile, are still struggling to regain their footing. Those same concerns as to returns on capital persist, while recent job letting in the sector – with around 90,000 US tech redundancies already announced for 2026 – suggest that company boards are focused on preserving their margins.

A global theme

For the last several years, returns from US stock markets – and by extension global stock markets – have been driven by a small handful of technology and consumer discretionary stocks. This was understandable given the ‘magnificent’ earnings growth they produced.

But the Magnificent 7 stocks aren’t the only beneficiaries of the AI buildout or the investor thirst to participate in it. Indeed, by the end of April this year, none of the so-called ‘Mag 7’ even featured in the top 30 performing S&P stocks year to date.

By that time, the top 15 companies in the S&P 500 Index were all vendors of semiconductors (chips) or computer networking equipment.

The AI buildout theme is also driving other major stock market indices – most notably in emerging markets. So far this year, the MSCI Emerging Market Index has gained well over 15% (to 29 April).

What’s most notable is that almost 90% of these gains have come from the technology sector, with just three names accounting for 60% of the total (in an index containing around 1,200 companies). These companies are TSMC (Taiwan Semiconductor Manufacturing Company), which alone accounts for 45% of Taiwan’s stock market, and the Korean giants Samsung Electronics and SK Hynix, which between them account for around 40% of Korea’s KOSPI Index.

AI-driven demand for the semiconductors produced by these two Korean leviathans has pushed Korea’s KOSPI Index into the stratosphere this year, along the way it’s helped Korea to replace the UK as the world’s eighth-largest stock market.

Source: Bloomberg data as at 26 April 2026. The Iran war commenced on 28 February 2026.

The value of investments and any income from them can fall and you may get back less than you invested.

Handelsbanken Wealth is a trading name of Handelsbanken Wealth & Asset Management Limited which is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business and is a wholly-owned subsidiary of Handelsbanken plc. Tax advice which does not contain any investment element is not regulated by the FCA. This document has been prepared by Handelsbanken Wealth for customers/potential customers who may have an interest in its services. The provision of this information does not constitute tax, pensions or investment advice.

Tax rates and legislation are subject to change. We cannot guarantee to inform you of any such changes and Handelsbanken Wealth accepts no responsibility for any inaccuracies or errors. Any levels of taxation referred to depend on individual circumstances and the value of tax reliefs are those which apply at 19 February 2026.

The value of the pension received when taking benefits from a pension will depend on various factors including, but not limited to, contributions made, charges and fees, tax treatments, annuity rates, investment performance. Professional advice should be taken before any course of action is pursued.

This does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. Handelsbanken Wealth cannot accept responsibility for the consequence of any action taken or failure to take action by a reader on the basis of the information provided. When we provide advice in relation to investment, our own investment management services will usually be recommended. When advice on pensions or other products outside an investment management relationship is required, we will recommend products chosen from a limited selection of providers that have been appointed on the basis of its judgement in their quality of service, investor protection, financial strength and, if relevant, their financial performance. As a result, any advice given by Handelsbanken Wealth in respect of retail investment products will be restricted as defined under the FCA rules.

This document has been issued by Handelsbanken Wealth.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340