Investment Team Handelsbanken Wealth

06 Jul 2026 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Fragile ceasefire triggers return of animal spirits

The start of April saw stock markets embark on an historic winning streak that ran right through to early June, triggered by the White House announcing a cessation of hostilities toward Iran. Against a backdrop of halting progress towards the reopening of the Straits of Hormuz, with oil prices easing over 40% in the second quarter, and the best US earnings season since 2021, stock markets progressed in leaps and bounds.

Led by technology stocks – most notably the memory-chip makers at the centre of the AI buildout – the S&P 500 Index of US companies enjoyed nine consecutive weekly gains. Meanwhile, Korea’s Kospi Index, home to two of the world’s largest memory-chip makers, doubled in the first half of the year, as did the Philadelphia Semiconductor (SOX) Index, which tracks the 30 biggest US chipmakers. The latter has already added over $5trn in value this year, putting it well on its way to its best year this century. Despite pausing for breath in June, as AI investor sentiment soured, global stock markets progressed just over 14% in the second quarter of 2026.

Star of the show: Emerging markets

Emerging market shares were the standout in the second quarter. Although it was virtually flat in June, the MSCI Emerging Market Index surged over 23% during the quarter. This meant that in the first half of the year, the index delivered 25.5% – twice the 12.7% delivered by the MSCI AC World Index.

Technology stocks now account for over 45% of the emerging markets index, but were responsible for over 90% of index returns year-to-date due to insatiable AI demand. Asia’s three largest chip fabricators, Taiwan Semiconductor (TSMC), and Korea’s Samsung Electronics and SK Hynix, have accounted for the lion’s share of returns this year, while transforming the fortunes of their local stock markets.

While TSMC has helped Taiwan’s stock market to gains of over 60%, the two Korean memory giants, both of which are now valued at over $1trn, helped Korea’s KOSPI Index to replace the UK as the world’s eighth-largest stock market during the second quarter.

Elsewhere in Asia, unceasing AI appetite has transformed the little-known memory-chip producer, Kioxia, into Japan’s largest company, displacing Toyota in the process.

A new sheriff in town

The arrival of Kevin Warsh as the new Chairman of the Federal Reserve (Fed) in June, initially sent shivers through the US government bond (Treasury) market. The taciturn new arrival was seen as being distinctly ‘hawkish’ – meaning he favours higher interest rates to fight inflation. This triggered the biggest sell-off in short-dated Treasuries in over a year, and the strengthening of the US dollar in expectation of future rate hikes.

Mr Warsh’s intention to deliver “price stability”, is a far cry from the candidate groomed by President Trump for his rate-cutting credentials. His ambitions for an ‘institutional reset’, encompassing changes to data sources, press communications, and forward guidance, also suggest a more opaque Fed going forward. Meanwhile, the clashing views among the central bank’s 18 rate-setters, hints that Mr Warsh’s Fed could be more fractured than that of his predecessor, Jerome Powell.

While the former could potentially lead to higher interest-rate volatility, the latter augurs for a period of ‘institutional inertia’ which should keep bond prices relatively stable. While observers wait to see the changes suggested by Mr Warsh’s various task forces, markets are already pricing in more than one 0.25% US interest-rate hike in 2026.

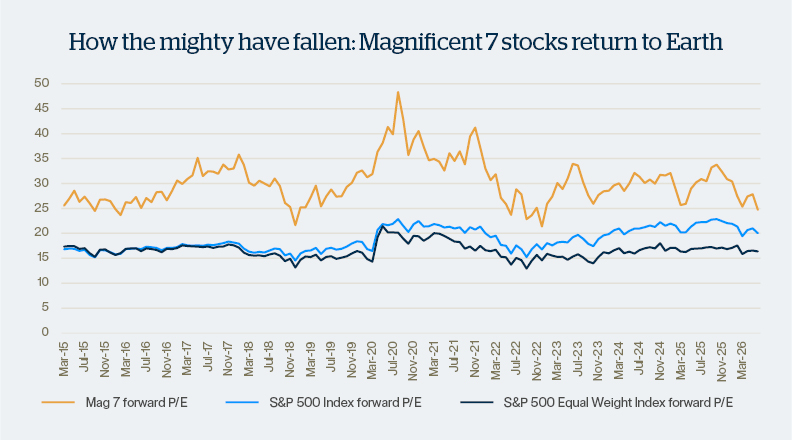

Source: FactSet, Handelsbanken Wealth. Data as at 30 June 2026.

The above chart neatly illustrates how the price to earnings (P/E) ratio for the Magnificent 7 (Mag 7) stocks has fallen to its lowest level, relative to the S&P 500 Index of US companies, for decade. (By dividing a company’s share price by its earnings per share (EPS), a P/E ratio expresses how much investors are willing to pay for every $1 of profit generated).

In this case, our chart shows that, despite the second quarter rally in stock markets being driven by AI fervour, the Mag 7 mostly missed out on the bonanza. This was focused on shares of companies supplying essential components and equipment to support the massive buildout of AI data centres. Standout US performers in 2026 include the likes of Sandisk, a memory-card maker which has gained some 600%, and other AI names such as Dell, Intel, Micron and Western Digital, which are around 200% up.

As the Mag 7 is picking up the tab for a large part of the AI buildout, it’s shed some $2trn in market value this year, underperforming the S&P 500 Index by some margin. At the half-way stage in 2026, only Alphabet (Google), Nvidia, Apple and Amazon had seen their shares progress with Meta, Microsoft and Tesla all nursing losses.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment funds.

![]()

Our stock market exposure

![]()

Our bond market exposure

The ‘alternative’ investment space covers an enormous universe of competing strategies and asset classes from gold, commodities and commercial property to specialist hedge funds that employ a diverse spectrum of strategies. Consequently, broad statements as to our view on the market as a whole are redundant.

In the alternatives space we hold only gold, a select group of hedge fund strategies, and a small position in commercial property.

Although we’re broadly underweight to alternatives, relative to our long-term average weighting, we have significant positions in gold, hedge funds, and a small but growing exposure to property assets where we’ve recently been reducing our underweight.

![]()

![]()

![]()

Our alternatives market exposure

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth is a trading name of Handelsbanken Wealth & Asset Management Limited which is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth, which is authorised and regulated by the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth or Handelsbanken ACD Limited: 25 Basinghall Street, London EC2V 5HA or by telephone on 01892 701803.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340