Investment Team Handelsbanken Wealth

31 Mar 2026 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Revving up: US company earnings

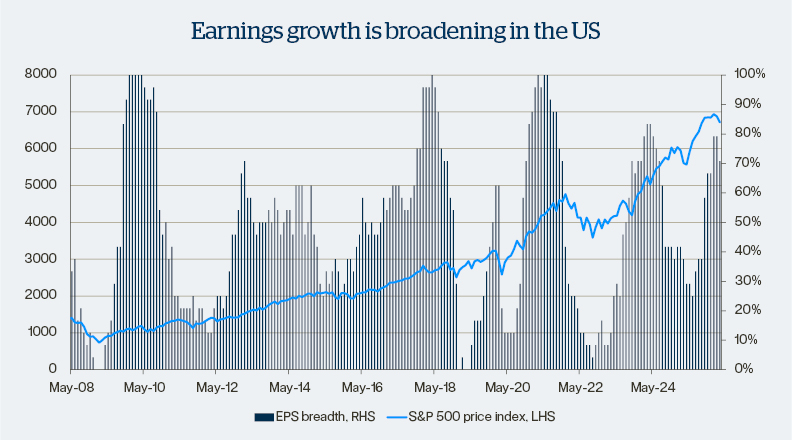

While the war in the Middle East has now passed its 15th day – statistically the average low point in markets following similar geopolitical upheavals – it naturally continues to be the focus of great attention. This has obscured both the profound levels US company earnings growth now forecast for 2026, and the fact that this earnings growth is broadening out right across the US market.

The latest forecasts from FactSet, show that earnings per share (EPS) growth for the S&P 500 Index of US companies has been substantially revised upward for the coming year. At the start of 2026, forecast EPS growth for the year ahead stood at 14%. It’s now expected to come in at a blistering 17% in the year to March 2027. Crucially for investors, over 70% of the S&P’s underlying industry subsectors are expected to see EPS acceleration this year (see this month’s chart).

Historically, when EPS growth broadens out like this, it’s provided a sustained boost for the market in question. This means that, unlike 2025, US market growth is no longer dependent on a small handful of mega-cap names.

Markets reverse direction as Iran war rages

Prior to the outbreak of the Iran war, US technology stocks, especially software companies, were on the backfoot. The software sector was down more than 30% from its high of late 2025. The Magnificent 7 (Mag 7), former darlings of the US stock market, had also struggled to gain traction.

At the start of 2026, investors were rotating into ‘old economy’, cyclical (meaning sensitive to the economic backdrop), smaller companies and value stocks. This favoured industrial, manufacturing, resources, energy and utility companies, at the expense of ‘new economy’ stocks exposed to the AI buildout. With tech stocks floundering, the broader US market also struggled due to its high weighting. This left the US in the dust over 2025 as investors favoured previously unloved regional markets such as the UK, Europe, Japan and emerging markets.

This rotation subsequently reversed with the onset of the Iran war. Since then, defensive, growth and energy stocks have flourished, as have US tech stocks. The Mag 7 has also been among the top performers while the US market is once again outperforming its peers, despite suffering losses.

UK gilts take hit from Iran war

UK government bonds, or gilts, have so far been one of the worst financial casualties of the Iran war. February’s solid gains were wiped away in March following the start of the Iran war, due to the risk it poses of a sustained, energy-driven inflation shock.

The ICE Bank of America Gilt index lost 4.8% in the first 20 days of March, putting gilts in negative territory for 2026, with the recent turmoil in the market being compared to that seen in the aftermath of the infamous Liz Truss mini-Budget crisis of 2022.

This has increased the cost of government borrowing and all but erased the UK Chancellor’s previous fiscal headroom of £20bn. At the time of writing, UK 10-year borrowing costs had already risen to an 18-year high, while the UK’s high-street lenders were increasing mortgage rates.

With gilt yields at historic highs (meaning their prices are at new lows) the market continues to be whip-sawed by President Trump’s changing rhetoric on the Iran war, a surprisingly ‘hawkish’ new tone from the Bank of England, and by the heavy presence of speculators unwinding their previous bets on UK rate cuts.

Source: FactSet, Handelsbanken Wealth. Data as at 21 January 2026.

The above chart shows how US company earnings growth (measured in earnings per share or EPS) is expanding, with over 70% of the underlying industry subsectors in the S&P 500 Index of US companies expected to see EPS growth in the year ahead.

Historically, this type of ‘broadening out’ in EPS growth provides a strong tailwind for any stock market fortunate enough to witness it.

The latest FactSet estimate for earnings growth in the S&P 500 Index stands at 17% for the year to March 2027. Even in a world where we still expect to see strong company earnings growth in the year ahead, especially in emerging markets, this figure stands out.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment funds.

![]()

Our stock market exposure

![]()

Our bond market exposure

The ‘alternative’ investment space covers an enormous universe of competing strategies and asset classes from commodities and commercial property to specialist hedge funds that employ a diverse spectrum of strategies. Consequently, broad statements as to our view on the market as a whole are redundant.

In the alternatives space we hold only gold, a select group of hedge fund strategies, and a small position in commercial property.

![]()

![]()

![]()

Our alternatives market exposure

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth is a trading name of Handelsbanken Wealth & Asset Management Limited which is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth, which is authorised and regulated by the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth or Handelsbanken ACD Limited: 25 Basinghall Street, London EC2V 5HA or by telephone on 01892 701803.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340