Investment Team Handelsbanken Wealth & Asset Management

21 Nov 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Investors have faced down an array of crises in 2025

It’s been a busy year for global news, with everything from US-centric trade wars to ongoing horrors in the Middle East. In the US – the world’s dominant market – there has also been a government shutdown (furloughing many government-paid employees and limiting government services), as well as various apparent attempts from the White House to infiltrate and influence the nominally independent US central bank. Despite all this headline-grabbing turbulence, investors have remained stoically optimistic, with most areas of financial markets broadly pushing higher throughout the year. (The weak oil price has been a highly visible exception.)

What’s with all the optimism?

Let’s be clear, 2025 hasn’t been without its wobbles, and there could well be more bumps in the road before the year is out. However, some of 2025’s nightmare spectres haven’t resulted in as much bad news as expected. For example, following President Trump’s infamous ‘Liberation Day’ announcements in April, most of the tariffs agreed with US trading partners have been much lower than Trump initially declared. The near-term impact of tariffs has also been less dramatic than feared (though of course the long-term effects are yet to be revealed), and markets always enjoy a good news surprise. Meanwhile, signals from both the oil price and inflation expectations tell us that investors have also moved on from issues in the Middle East for the time being. What’s more, central banks around the developed world are broadly cutting interest rates, and this has historically been a positive development for economic growth, and for riskier asset types like shares.

Trouble on home shores could be one to watch

On UK soil, the picture is trickier. The Bank of England’s decision-making committee cut rates in August, but has since opted to hold rates steady at 4%. The narrowness of the committee’s November vote was surprising to markets: the members voted 4 aside to hold or cut rates, with the governor of the bank – Andrew Bailey – casting the deciding vote to keep rates at their current levels. Governor Bailey noted that for further rate cuts to happen, he would need to see inflation continue to fall back, and has signalled a cautious approach to future interest rate cuts. Inflation figures for October (measured by CPI) were released in mid-November, and showed that prices in the UK had risen by 3.6% over the previous year (a little lower than in September, when CPI was 3.8%). As a reminder, the Bank of England’s goal for inflation is 2%. Our view remains that the Bank may need to cut rates by more than the market expects, in order to support growth in the UK economy.

How are our investment strategies positioned for the next chapter?

We’ve spent the past 18 months or so simplifying our investment positions and making them exceptionally ‘liquid’ – ready to move easily if need be. Our investment strategies are well-diversified across different types of financial assets, including our stock market positioning, where we’ve previously slightly reduced our exposure to the choppy US market.

As we’re sure our clients already know, investing always means exposing your capital to the possibility of both rises and falls in financial markets, presenting both risks and opportunities. It’s our privilege to help you understand more about this, so if you would like more information, please do get in touch.

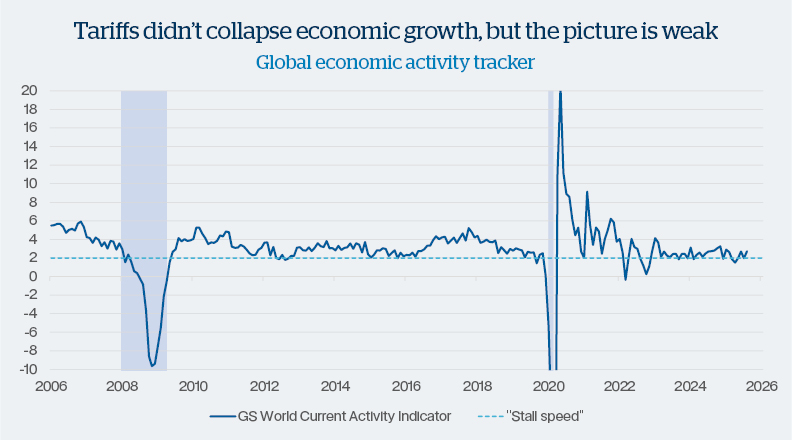

Source: Goldman Sachs, Bloomberg, Macrobond

The chart above tracks economic activity in the global economy. ‘Stall speed’ of 2% is marked on the chart, and signifies a low level of overall growth, below which we believe the global economy would show signs of real struggle.

You can see that following the initial COVID-19 pandemic shock in 2020, turbulence in global economic growth has been settling down. Unfortunately, it’s been settling at rather a low level – close to stall speed.

Weak patches of economic activity do happen, but markets will be closely watching to see if this is anything more worrying. Uncertainties around issues like global trade are not useful for confidence and growth, so news like the recent 12-month tariff truce between the US and China is helpful for this picture.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment funds.

At the time of this update, we are 'neutral' stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset funds currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset funds currently hold a proportion of investments in bond markets which is consistent with our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset funds currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 25 Basinghall Street, London EC2V 5HA or by telephone on 01892 701803.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340